Turn Less into More: Behavioural design lessons from trusted saving solutions in the informal economy.

A #BeFiFaculty post by Marna Landman (PhD, MBA, FCCA), Behavioural Economist, Beam Insights

#BeFiFaculty = The Behavioural Finance Faculty is a group of GAABS members who come together regularly to share best practice applications of behavioural science to real-world financial challenges.

Saving for a rainy day has always been difficult. Timeless saving lessons passed down through fables (e.g. the Ant and the Grasshopper from Aesop’s Fables) and biblical parables (e.g. Parable of the Talents, Matthew 25:14-30) remain relevant today and financial advice is now more accessible than ever. Despite advice available from social media, self-help books, financial advisors and evidence-based scientific research, the problem of inadequate household saving rates is wicked and persists across the globe (OECD).

To address this problem of low household and personal saving rates, research spans multiple disciplines from behavioural studies (e.g., on habit formation and biases like present bias, status quo and confirmation bias) to the implementation of commitment saving devices (like savings accounts) and financial literacy programmes. However, it is abundantly clear that no “quick fix” or widely generalisable solutions exists. Complexity, contextual differences (e.g. cultural nuances, varying micro- and macro-economic environments) and a wide variety of personal factors influence the saving decisions of individuals.

Economic measures on saving (such as saving rates) are derived almost exclusively from the formal sector and overlook savings of “unbanked” individuals in informal economies, mostly because it is near impossible to measure. But what if practical solutions that mobilise savings effectively and at a low cost already exist in the informal economy? Saving groups, for example, are trusted saving solutions and very popular under conditions of financial scarcity. This social construct is an informal commitment savings device that provides rich insights on saving behaviour in general.

Saving groups are, for example, also known as “tanda” in Latin America, “bishi” in India, “gam’eya” in the Middle East, and “stokvels” in South Africa.

Saving in the Informal Economy

Saving groups are informal associations where members pool their funds to save for common purposes and to support each other (with loans and in other non-financial ways), by fostering a sense of community. These groups originated in contexts where limited or no access to traditional financial services existed, such as low- to mid-income developing countries and informal economies. Saving groups are usually governed through a constitution with well-defined rules and procedures for saving and borrowing to ensure transparency and democratic decision-making on the pooled funds.

Verbatim (translated) interview quote from a saving group:

“The reason why we decided to form this group is that we can’t do things on our own as people, but if you team up with the others and put together our money, you are even able to borrow money for a sizeable amount and do big things that you would not have been able to do yourself.”

(Landman & Mtombeni 2021, p.7).

The number of people participating in saving groups globally are likely understated due to a lack of reliable data and statistics on informal economies, especially in Africa. In South Africa alone, best estimates suggest more than 11 million individuals participate in approximately 800,000 saving groups, which circulates an estimated ZAR50 billion (±USD2.8 billion) annually. In this market, saving groups (known as stokvels) are established to save for purposes that range from bulk grocery purchases to property investment clubs. Saving groups are fast becoming more financially sophisticated, regulated and popular for purposes beyond subsistence savings.

Transferable insights from informal saving groups

What can we learn from informal saving products to design behaviourally informed saving products and services for the formal economy? Despite the rich and inherent behavioural design of saving groups, this saving device has not really been studied holistically. Research on saving groups have mostly focused on experimenting with tailored interventions to increase savings in a particular context or for a specific purpose (e.g. development programs).

Interviews with individual members and saving groups in South Africa offers a deeper understanding of its behavioural mechanisms and features (Landman & Mtombeni, 2021). The outcome is a practical, behavioural design framework (Figure 1) for financial advisors and developers of saving solutions (e.g. to adapt services, products and applications) in the formal economy.

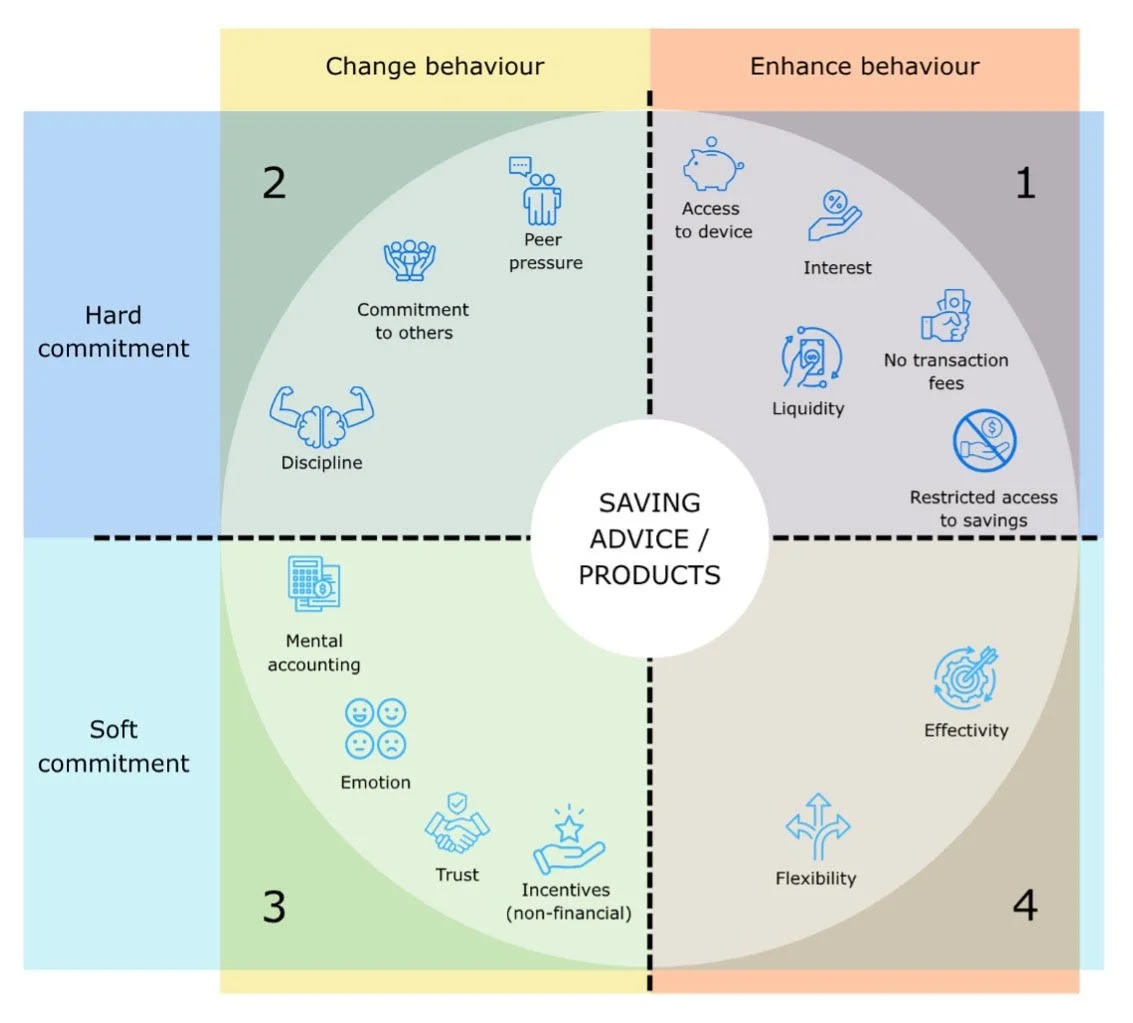

Figure 1. Behavioural Design Framework

The framework illustrates that members of saving groups identified peer pressure, a commitment/obligation toward others, and discipline (self-control) as key features to increasing saving behaviour (Quadrant 2). However, softer commitment features such as mental accounting (mental earmarking of a specific amount for saving, mainly to overcome self-control problems and to limit the money available for spending), emotional connection, trust, and non-financial incentives were considered to be equally effective (Quadrant 3). It seems that saving groups are effective to change saving behaviour and mobilise savings because they combine and leverage these seven features successfully.

Characteristics of saving groups that are valued by members and believed to enhance their saving behaviour includes access (geographical proximity and/or low-cost access) to the group, ability to earn interest on savings, or being charged interest penalties when deviating from group norms and rules. Additionally, a lack of transaction fees, liquidity for emergencies in the form of short-term loans and restricted access to prevent unnecessary withdrawals, are non-negotiable features (Quadrant 1). Members believe that saving groups are effective in helping them to save because of flexibility allowed for financial shocks that often occur in their context (Quadrant 4). These seven features that enhance saving behaviour are likely features that increase member (customer) retention, as they are explicitly and uniformly preferred.

This framework suggests that different soft and hard commitment features of saving solutions have different effects on saving behaviour. Hard commitment features rely on force, rules, penalties, or terms and conditions to function effectively. On the other hand, soft commitment features use an abstract approach to influence (change or enhance) saving behaviour by focusing on customers’ mindsets, emotions and perceptions. Features that change behaviour are those that typically increase initial adoption of solutions, while those that enhance behaviour are equally necessary to ensure subsequent customer retention. Much can be learned and replicated from saving groups as effective, low-cost commitment saving devices. It is likely that their effectivity and popularity are attributable to behavioural design and how all its features operate collectively to improve saving behaviour. We recommend testing this behavioural design framework to personalise and expand advisory services or saving product design. Ultimately, this framework suggests interventions to simplify individuals’ saving behaviour even when experiencing financial scarcity - like most of us do from time to time.

Conclusion

New insights can be gained from looking at existing, wicked problems from a different behavioural angle. Using a “bottom-up approach” by exploring basic questions such as “What already works for whom, where and why?”, we might discover fresh ideas and pathways to personal saving solutions for greater financial resilience in diverse contexts.