The Hexagon Framework: A Behavioral Approach to Building Financial Wellbeing

A #BeFiFaculty post by

Pepa Vilaplana, Financial Health Expert, BeWay Consulting

Silvia Cottone, Behavioral Marketing Consultant, BeWay Consulting

GAABS Behavioural Finance Faculty Members

The Behavioural Finance Faculty is a group of GAABS members who come together regularly to share best practice applications of behavioural science to real-world financial challenges.

In a world where financial decisions are increasingly complex and emotionally charged, even one choice can shape long‑term wellbeing.

Imagine you are a student and need a loan to finance your studies—an investment that could open the door to a more promising professional future. In front of you, there are two paths:

A “good” debt: This option offers a moderate interest rate and a clear repayment plan, tailored to the student’s financial capacity. It enables progress toward personal goals without jeopardizing stability.

A “bad” debt: This option almost uses the entire limit of your credit card, making only minimum payments, with no clear strategy and high interest rates. This approach risks undermining long-term financial wellbeing.

The impact of these choices extends far beyond the immediate balance sheet. The way we manage debt today shapes our ability to make decisions aligned with our values and future aspirations. Managing money isn’t just about knowing the numbers—it’s about navigating emotions, behaviors, and decisions that shape our financial outcomes. Conscious, strategic choices are the foundation for building a healthier and more resilient financial life.

Financial health is directly related to people's overall well-being. When positive, it reduces stress and anxiety, allows them to make better decisions and achieve their life goals. Supporting financial health is no longer an optional business strategy. It's a fundamental path to maintaining the stability of individuals and businesses.

Although financial institutions can help individuals achieve better financial well-being through optimizing their products, it is also important that people understand the factors behind it and know how to act to achieve positive financial health.

This is one of the missions at BeWay, and thanks to our team of experts, we’ve developed the Financial Wellbeing Hexagon, a behavioral science-based framework designed to translate abstract financial principles into concrete, actionable behaviors that anyone can implement.

In this article, we introduce the six core pillars of financial wellbeing and offer practical guidance to help individuals build a healthier, more resilient financial life.

What Is Financial Wellbeing, Really?

Traditional approaches (Joo, 2008) describe financial wellbeing as a combination of objective status (one’s actual financial situation), subjective perception (how one feels about it), and behavioral patterns (what one does with their money). Yet most financial tools focus only on the first aspects—your account balances, income, or debt. This leaves out the psychological and behavioral realities that truly drive change and help individuals manage their current financial obligations and have confidence in their financial future.

After reviewed several theoretical frameworks on financial wellbeing and the available empirical evidence, we adapted the information into practical and actionable recommendations for individuals.

The Hexagon Framework (below) is a guide informed by financial consulting experts, designed to help maintain a high score across the key components that should be considered to optimize financial wellbeing: meeting present obligations, building resilience against unexpected events, and achieving medium- and long-term goals. Indeed, true financial wellbeing is a dynamic state that combines:

Feeling secure in the present

Being prepared for the unexpected

Building a future aligned with one´s values and goals

Each component of the hexagon is inspired by evidence-based dimensions, enriched by our consulting experience, ensuring that our recommendations are grounded in solid knowledge.

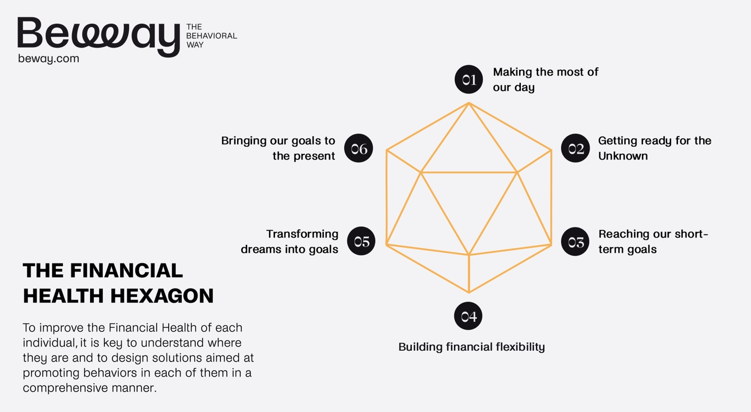

The Financial Health Hexagon

The Hexagon Framework organizes financial wellbeing into six behavioral pillars. To improve everyone's financial wellbeing, it's key to understanding their current situation and design solutions aimed at promoting holistic behaviors. Each pillar is a lever you can act on—regardless of your income level, financial knowledge, or status.

1. Optimize Daily Spending

Goal: Maximize the value you get from your day-to-day income.

Why it matters: Your budget is your most immediate source of financial control. But it's not just about tracking expenses—it’s about spending in alignment with your personal values.

Try this:

Separate your expenses into “must-haves” and “nice-to-haves.”

Use mental accounting (creating digital envelopes or categories) to allocate spending.

Automate your fixed costs and limit your discretionary ones.

Behavioral tip: People often underestimate small, recurring expenses. Use reminders or budgeting apps to bring visibility to “invisible” spending.

2. Prepare for the Unexpected

Goal: Build a buffer to handle financial shocks.

Why it matters: Life is unpredictable. Having a liquidity cushion reduces stress and prevents costly decisions like high-interest borrowing.

Try this:

Start with a micro-emergency fund (e.g., $200).

Automate transfers to a separate savings account labeled “emergency.”

Reframe this fund not as “money you’re losing access to,” but as “freedom insurance.”

Behavioral tip: People tend to procrastinate building emergency savings. Labeling the fund (“For Future Me” or “When Life Happens”) makes it feel more purposeful.

3. Build Short-Term Savings Habits

Goal: Reach near-term goals with consistent savings.

Why it matters: Small wins reinforce financial discipline and keep motivation high. This is where savings becomes a habit—not a sacrifice.

Try this:

Define a specific goal (e.g., $500 for a trip) and a timeline.

Use automatic savings rules—like saving a fixed amount every payday.

Apply the “pay yourself first” principle, i.e., prioritize saving a portion of your income before spending it on other expenses.

Behavioral tip: The pain of saving decreases when it’s automated. Pre-committing helps overcome present bias.

4. Develop Financial Flexibility

Goal: Access the right tools to adapt and grow.

Why it matters: Flexibility is what lets you respond to opportunity—not just avoid crisis. It means using a mix of financial products—insurance, savings, loans, and investments—in a coordinated way.

Try this:

Periodically review your financial “toolbox.” What do you need to add (e.g., insurance)? What’s outdated?

Understand the purpose of each product: protection, growth, liquidity, etc.

Seek professional advice if unsure about financial decisions.

Behavioral tip: Behavioral inertia keeps many people from switching or updating financial tools. Set an annual “financial checkup” date.

5. Invest in Long-Term Goals

Goal: Turn dreams into plans through investment.

Why it matters: Investing isn’t just for the wealthy. It’s about ensuring your future self can afford your goals—from retirement to education to entrepreneurship.

Try this:

Choose an investment strategy aligned with your values and risk tolerance.

Set a monthly contribution, no matter how small.

Focus on the identity shift—you’re not just a saver, you’re an investor.

Behavioral tip: Reframing long-term investing as part of your life story—“I’m building my future”—helps make delayed rewards more tangible.

6. Use Credit Strategically

Goal: Bring your future goals into the present, responsibly.

Why it matters: Not all debt is bad. Strategic use of credit—like education or mortgage loans—can support upward mobility. But poor credit habits can erode wellbeing.

Try this:

Know the difference between good and bad debt.

Keep track of your credit utilization ratio (stay below 30% of your available credit).

Avoid minimum payments—automate more than the minimum if possible.

Behavioral tip: You are more likely to make payments on time when reminded of consequences (like fees or score drops) and benefits (like travel rewards or improved credit).

Bringing the Hexagon to Life

You don’t need to master all six pillars at once. Start where you are. Choose one of the pillars to focus on for the next 30 days. Track your progress. Celebrate small wins.

Here’s a simple reflection prompt:

Which area of the Hexagon feels strongest for me today?

Which area, if improved, would have the biggest impact on my overall wellbeing?

The Hexagon is not a rigid model—it’s a guide. A framework to structure your financial life around behaviors that compound over time.

Limitation & context consideration

Like any behavioral framework, the Financial Wellbeing Hexagon has limitations that should inform its interpretation and use.

First, although the framework is grounded in established literature and the practical expertise of our consulting team, it still requires empirical validation. In particular, the relative contribution—or weight—of each hexagon dimension to overall financial wellbeing has not yet been quantified. Future research is needed to assess how strongly each pillar influences outcomes and whether their impact varies across populations.

Second, the Hexagon places a strong emphasis on financial behavior in relation to financial products—such as savings accounts, insurance, credit, or investment tools. While this focus allows for actionable and concrete recommendations, it also means that the framework assumes a minimum level of financial inclusion and access to formal financial services. In contexts where such products are limited, inaccessible, or culturally misaligned, other sets of recommendations may be more relevant or necessary. For example, communities with low financial inclusion may require more foundational support around informal savings, social safety nets, or basic financial literacy before the Hexagon can be effectively applied.

Third, financial behaviors are strongly shaped by cultural norms, socioeconomic conditions, and structural constraints. Concepts such as budgeting, saving, debt, or investing can take on different meanings depending on context. The Hexagon should therefore be adapted—not applied uniformly—across countries, cultures, and demographic groups.

Finally, financial wellbeing is inherently dynamic. Individuals’ priorities, risks, access to resources, and emotional states evolve over time. The Hexagon is not meant to be a one-time diagnostic tool, but rather a recurring framework for reflection and adjustment.

Practitioners and organizations should consider the framework as a structured starting point for understanding and supporting individuals, complementing it with qualitative insights and contextual knowledge whenever possible.

From Awareness to Action: How Organizations Can Apply the Framework

The true value of the Financial Wellbeing Hexagon emerges when organizations move beyond understanding the conceptual model and begin testing, applying, and operationalizing it in real-world contexts.

The Hexagon can serve as a practical blueprint for guiding decisions, shaping behavioral interventions, and embedding financial wellbeing into business strategy.

1. Testing the Hexagon in Specific Contexts

One of the most effective ways to leverage the framework is by testing its recommendations within specific cultural, market, or demographic contexts. Because financial behaviors and constraints differ across populations, organizations can use the Hexagon as a structured hypothesis:

Which behaviors matter most here?

Which interventions drive measurable change?

Through pilots, experiments, and behavioral diagnostics, institutions can validate which pillars have the strongest local relevance and refine the recommendations accordingly. This process not only strengthens the evidence behind the model but also ensures its contextual fit and effectiveness.

2. Using the Hexagon to Design Policies and Behavioral Interventions

The framework also functions as a design tool. Policymakers, NGOs, and financial service providers can rely on the six pillars to craft interventions that promote specific financial behaviors, such as building emergency buffers, improving credit practices, or supporting consistent savings habits.

By organizing policies around these behavioral levers, organizations can create initiatives that are clearer, more targeted, and more aligned with how people actually make financial decisions. The Hexagon provides a practical language that helps translate abstract wellbeing principles into actionable program features.

3. Setting Business Goals and KPIs Focused on Financial Health

For private-sector organizations—especially banks, fintechs, and insurers—the Hexagon offers a way to connect customer wellbeing with business strategy. By grounding goals in observable behaviors from the framework, companies can create KPIs that reflect progress in financial health, such as improved savings consistency, reduced risky debt, or increased uptake of appropriate financial tools.

This shift encourages institutions to focus not only on product usage but on meaningful, long-term outcomes for their customers. It also opens the door to new value propositions: products, communication strategies, and services that genuinely enhance financial wellbeing while supporting sustainable business growth.

References

1. Consumer Financial Protection Bureau. (2017). Financial well-being: The goal of financial education. https://www.consumerfinance.gov/data-research/research-reports/financial-well-being/

2. Lomas, T. (2019). The flavors of love: A cross-cultural lexical analysis. Journal of Happiness Studies, 20(3), 773–799. https://doi.org/10.1007/s10902-019-00145-3

4. Lomas, T., & VanderWeele, T. J. (2023). The flavors of flourishing: A cross-cultural lexical analysis. Journal of Happiness Studies, 24(6), 2671–2693. https://doi.org/10.1007/s10902-023-00697-5

5. Organisation for Economic Co-operation and Development (OECD). (2023). G20 policy note on financial well-being. OECD Publishing. https://www.oecd.org/en/publications/g20-policy-note-on-financial-well-being_7332c99d-en.html